Crypto & retirement

Crypto & retirement

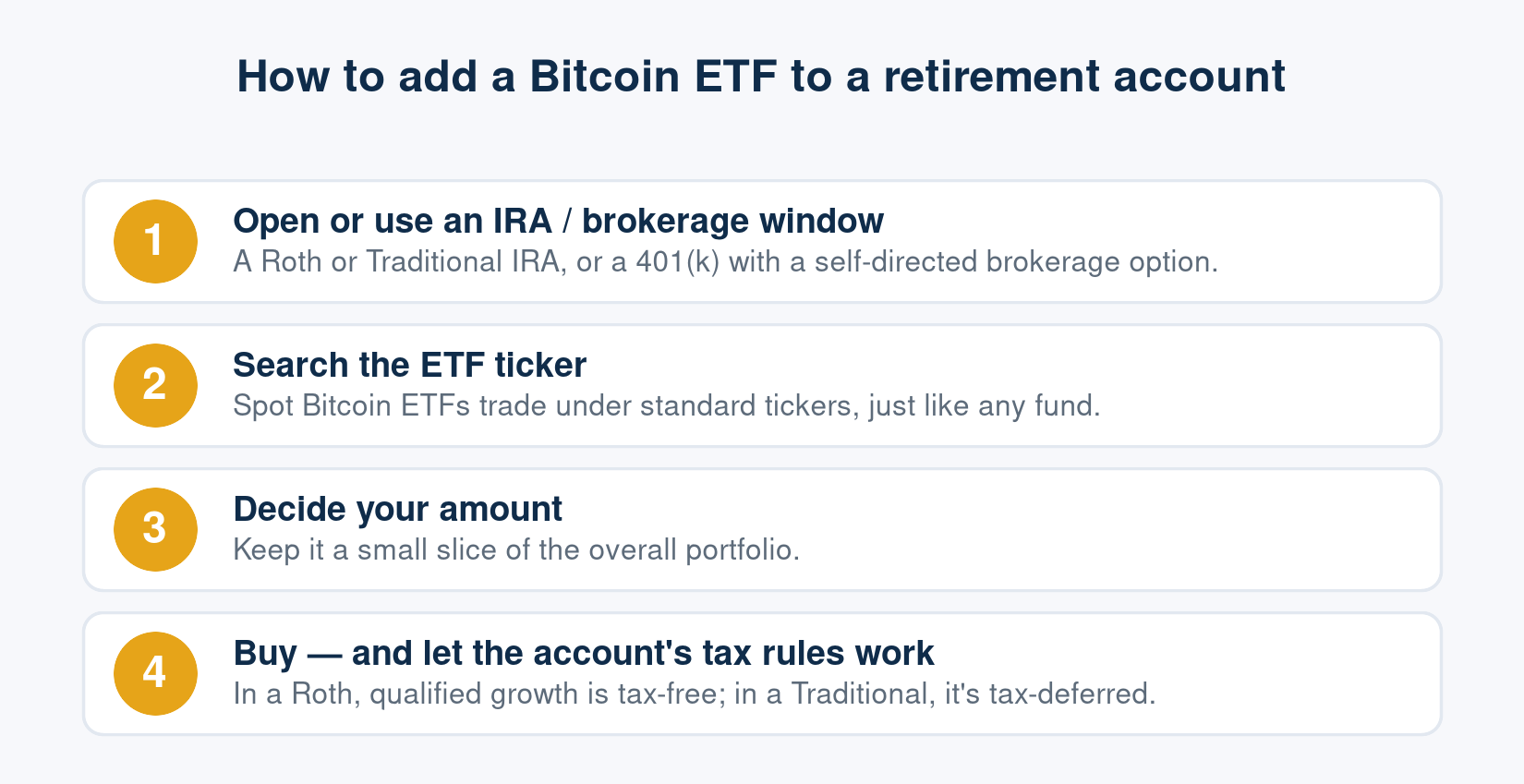

Bitcoin ETFs in Your IRA or 401(k)

Spot Bitcoin ETFs let you add crypto to an IRA or 401(k) as easily as buying a stock — no wallets, no keys, no special custodian. Here's how they work, how they compare to owning coins directly, and how to buy one inside a retirement account.

For years, the hard part of owning crypto in a retirement account was the plumbing: special custodians, private keys, and unfamiliar platforms. Spot Bitcoin ETFs erased most of that friction.

What a spot Bitcoin ETF actually is

A spot Bitcoin ETF holds real Bitcoin in custody and issues shares that track its price. (That's different from the older futures ETFs, which tracked contracts rather than coins.) When the SEC approved spot Bitcoin ETFs in January 2024, it gave ordinary investors a regulated, familiar way to own Bitcoin exposure through a normal brokerage account.

Why it's the simplest retirement route

- Buy it in the IRA you already have — Roth or Traditional — like any stock or fund.

- No private keys to lose and no separate crypto custodian to vet.

- The account's tax rules apply: Roth = tax-free qualified growth, Traditional = tax-deferred.

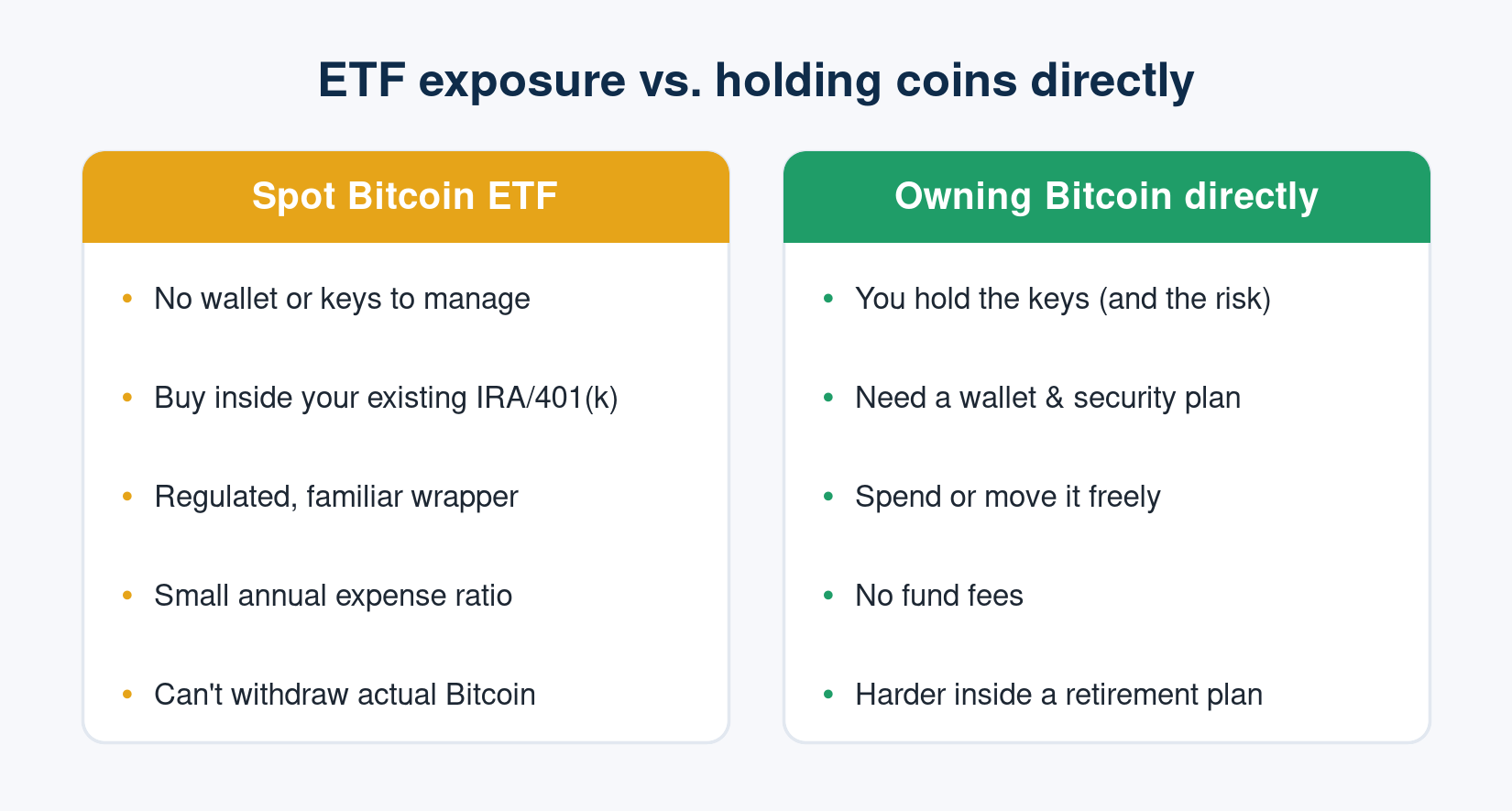

ETF exposure vs. owning coins directly

An ETF isn't the same as owning Bitcoin outright. You can't send it, spend it, or self-custody it — you own a share that tracks the price. For a retirement investor who just wants exposure and simplicity, that's usually a fair trade. For someone who wants to actually use Bitcoin, direct ownership (or a self-directed crypto IRA) fits better.

What about a 401(k)?

Most 401(k) menus don't list crypto directly, because the lineup is chosen by your employer. But there are two ways in:

- A self-directed brokerage window. Many plans offer one, and it can buy ETFs — including spot Bitcoin ETFs. This is the most common practical path.

- A direct Bitcoin option. A few large providers have begun offering one, though availability is limited and often capped at a small share of contributions.

The U.S. Department of Labor has urged plan fiduciaries to use caution before adding crypto, so don't be surprised if your plan doesn't offer it.

The costs and trade-offs

- Expense ratio: ETFs charge a small annual fee. Over decades it adds up, so compare funds.

- No self-custody: you can't withdraw the underlying Bitcoin.

- Still volatile: the wrapper is convenient, but the price swings are exactly the same.

The bottom line

If you want crypto in a retirement account and value simplicity and safety over holding the actual coins, a spot Bitcoin ETF in your IRA — ideally a Roth, for tax-free growth — is the most straightforward option available today. Just keep the position small and capture your employer match first.

Educational information only — not financial, tax, or legal advice. Crypto is volatile and speculative; consult a qualified professional about your situation.

Comments

No comments yet — be the first to share your thoughts.

Sign in or create an account to comment.