Crypto & retirement

Crypto & retirement

Crypto Estate Planning: Passing Bitcoin to Your Heirs

Crypto's biggest inheritance risk isn't taxes — it's lost access. This guide covers building a secure access plan, the trade-off between self-custody and custodial accounts, beneficiary designations, the step-up in basis, and how to make sure your heirs can actually recover what you leave them.

With a bank account, your heirs can walk into a branch with a death certificate. With self-custodied crypto, there is no branch, no password reset, and no customer-service line. If the keys are lost, the coins are lost — permanently. That makes access planning the true heart of crypto estate planning.

The unique risk: lost keys

Untold amounts of Bitcoin are already stranded forever because owners died or lost access without a plan. Your heirs can't inherit what they can't reach. Before anything else, solve the access problem.

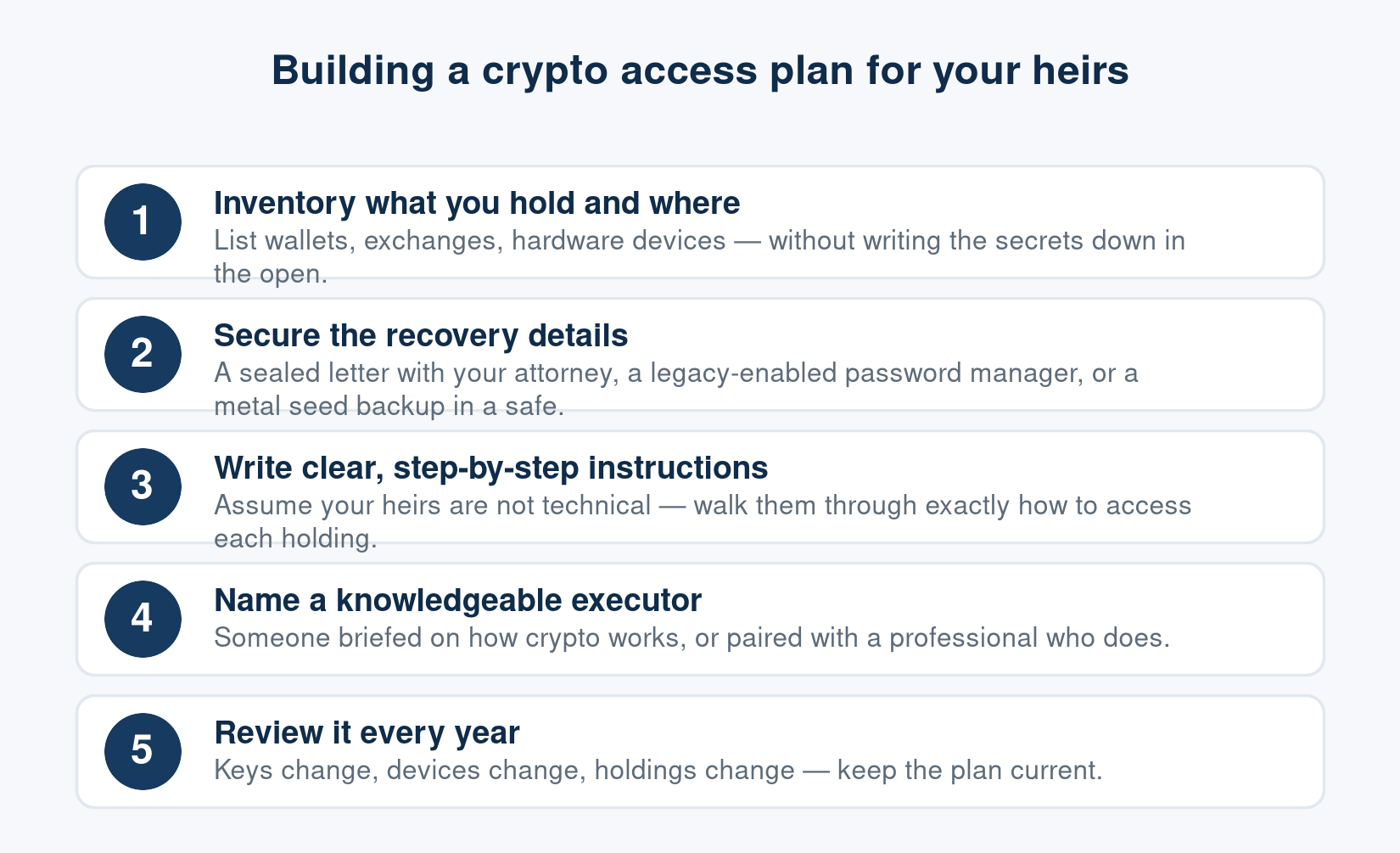

Create an access plan — securely

The goal is to make recovery possible for your heirs without exposing your secrets while you're alive. A few guardrails:

- Never put seed phrases or private keys in your will. A will typically becomes a public document.

- Do document where things are — which wallets, which exchanges, which hardware devices — and how to access each.

- Store the secrets safely: a sealed letter with an attorney, a password manager with a legacy/emergency-access feature, or a metal seed backup in a safe deposit box.

- Write for a non-expert. Assume the person recovering it has never used a hardware wallet.

Self-custody vs. custodial accounts

Crypto held at an exchange or inside a crypto IRA can name a beneficiary and transfers much more like a traditional account — often the single biggest simplification for inheritance. The trade-off is that you give up some self-custody. Many families use a mix: self-custody for control during life, and clear beneficiary designations or a documented plan so heirs aren't left stranded.

The tax angle: step-up in basis

There's good news on taxes. Inherited crypto held in a taxable account generally receives a step-up in cost basis to its fair-market value on the date of death. That can erase the built-in capital gain — heirs who sell shortly after inheriting may owe little or nothing on the appreciation that happened during your lifetime. Crypto in a Roth IRA can pass tax-free as well, subject to the rules for inherited retirement accounts.

Consider more advanced tools

For larger holdings, options like multi-signature wallets (which require multiple keys to move funds), specialized crypto-inheritance services, or a trust can add security and control. These add complexity, so weigh them against the size of what you're protecting.

The bottom line

Crypto estate planning is really two jobs: make sure your heirs can access the assets, and make the transfer as tax-efficient as possible. Build a secure, documented access plan, use beneficiary designations where you can, and lean on the step-up in basis. Work with an estate attorney and tax professional — this is general information, not legal or tax advice.

Educational information only — not financial, tax, or legal advice. Crypto is volatile and speculative; consult a qualified professional about your situation.

Comments

No comments yet — be the first to share your thoughts.

Sign in or create an account to comment.