Crypto & retirement

Crypto & retirement

Can You Hold Crypto in an IRA?

You can hold Bitcoin and other crypto in an IRA, and it can be one of the most tax-efficient ways to own it. This guide covers both routes — a self-directed crypto IRA and a spot ETF in a normal IRA — plus fees, rules, and the mistakes that trigger taxes.

Owning crypto in a regular taxable account means every sale or trade is a taxable event, and record-keeping can be brutal. Holding it inside an IRA changes that entirely: the account's tax shelter does the heavy lifting. The question isn't really can you — it's which way makes sense for you.

The short answer: yes

The IRS treats cryptocurrency as property, and property can live inside an IRA. When it does, your crypto inherits the account's tax treatment — tax-deferred growth in a Traditional IRA, or tax-free qualified growth in a Roth. Trades inside the account don't generate a tax bill each time you rebalance.

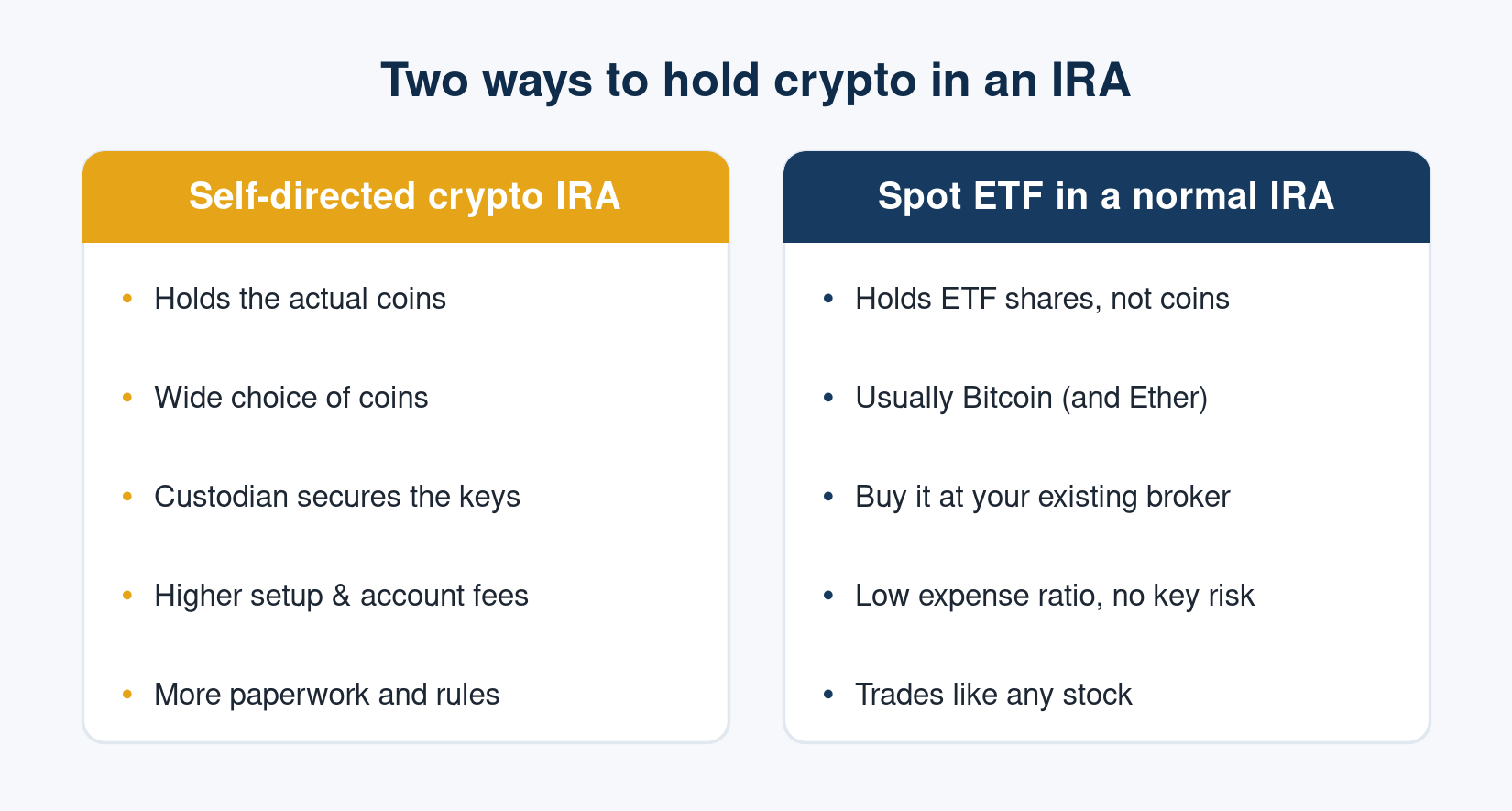

There are two very different ways to get there, and picking the right one matters more than most people realize.

Path 1: a self-directed crypto IRA

A self-directed IRA (SDIRA) is an IRA that can hold alternative assets — including crypto — through a specialized custodian. The custodian handles storage, security, and the IRS reporting, and you direct what's bought and sold.

What's good about it

- You own real crypto, not a proxy — and often a wide menu of coins beyond Bitcoin.

- Everything stays inside the IRA's tax shelter.

- Custody and cold storage are handled by professionals.

What to watch

- Fees are typically higher: setup fees, annual account fees, and sometimes trading spreads.

- You must follow strict IRA rules — no self-dealing, no personal use of the assets.

- Not every custodian is equal; check security practices, insurance, and reputation.

Path 2: a spot crypto ETF in a normal IRA

Since spot Bitcoin ETFs were approved in January 2024 (and spot Ether ETFs later that year), you can now get crypto exposure inside your existing brokerage IRA without any special account. You buy the ETF the same way you'd buy an index fund.

For most retirement savers, this is the simplest, lowest-friction option: no separate custodian, no private keys to secure, and the familiar comfort of a regulated product inside an account you already have. The trade-off is a small annual expense ratio and the fact that you hold shares, not spendable coins.

A critical rule: never take personal custody

This is where people get burned. Crypto owned by your IRA must stay with the account's custodian — you cannot move IRA-owned coins to your own hardware wallet. In the McNulty v. Commissioner tax-court case, an investor who did exactly that was treated as having taken a full taxable distribution of the account, with taxes and penalties to match.

The rule of thumb: if it's in your IRA, the custodian holds the keys — not you.

Which should you choose?

- Want simplicity and low cost? A spot Bitcoin ETF in your existing IRA is hard to beat.

- Want to hold actual coins or a wider range of assets? A self-directed crypto IRA is the tool, if you accept the fees and rules.

- Either way, decide between Traditional (tax-deferred) and Roth (tax-free) based on your tax situation.

Whatever you choose, size the position sensibly — an IRA doesn't make a volatile asset any less volatile.

Educational information only — not financial, tax, or legal advice. Crypto is volatile and speculative; consult a qualified professional about your situation.

Comments

No comments yet — be the first to share your thoughts.

Sign in or create an account to comment.