Careers

Careers

Retirement Planning for Food Preparation Workers

As a food preparation worker, you earn a U.S. median of about $31,000 a year. Retirement can feel far off — or even out of reach — on that income, but a comfortable one is very doable if you use the right account and start the habit early. Here's a plain-English, no-jargon plan for food preparation workers.

Your typical retirement setup

Kitchen and food-prep jobs rarely include a retirement plan, which makes a Roth IRA your main tool. You open it yourself, contribute a little each payday, and let decades of tax-free growth do the work. If a larger employer offers a 401(k) match, take that first — it's free money.

The Saver's Credit: free money for saving

Here's a benefit most people in this income range miss. If your household income is modest, the IRS gives you the Saver's Credit — a tax credit worth 10%, 20%, or even 50% of what you put into a retirement account (up to a limit), on top of the account's own tax advantages. You contribute to a Roth IRA or a 401(k), file IRS Form 8880, and the government effectively chips in. It's one of the best deals in the tax code, and it's aimed squarely at working people.

What to watch as a food preparation worker

- Save a set amount every payday. Pick a small, fixed number and automate it so saving happens without a decision.

- Watch for a 401(k) at bigger employers. Chains and institutional kitchens sometimes offer one with a match — always claim the full match.

- Keep costs low. Put your Roth IRA in a simple, low-cost index fund and leave it alone.

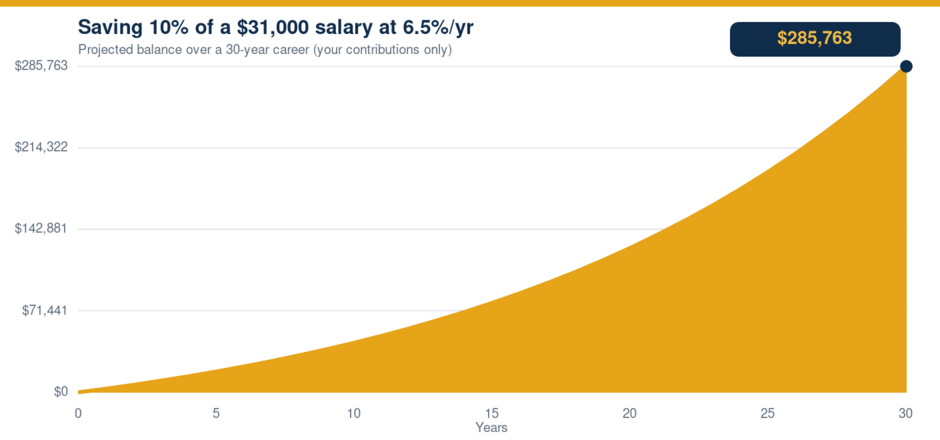

Even small amounts add up

You don't need a big salary to end up with a real nest egg — you need time. Here's what setting aside about 10% of a $31,000 salary — roughly $258 a month — could grow into over a 30-year career at about a 6.5% average annual return:

That's roughly $285,763 from steady saving alone. If that number surprises you, that's the power of compounding: small, consistent contributions turn into serious money when you give them decades to grow.

Common mistakes to avoid

- Thinking you earn too little to save. Even $20–$50 a paycheck, started early, becomes a meaningful sum. Waiting is the real mistake.

- Leaving a match on the table. If your employer offers any 401(k) match, that's free money — grab it first.

- Cashing out when you switch jobs. Roll old accounts over instead of cashing them out and losing money to taxes and penalties.

- Skipping the Saver's Credit. If you qualify and don't claim it, you're leaving a tax refund on the table.

Your game plan

- If your job offers a 401(k) match, contribute enough to get all of it.

- Open a Roth IRA and set up an automatic transfer every payday — even a small one.

- Claim the Saver's Credit at tax time (Form 8880) if your income qualifies.

- Raise your contribution a little whenever your pay goes up.

- Keep it in a low-cost, broadly diversified index fund and leave it alone.

None of this is financial advice — check the details for your own situation. But the message is simple and hopeful: a comfortable retirement isn't only for high earners. For food preparation workers, starting early, saving a little every payday, and letting time do the compounding is what gets you there.

Comments

No comments yet — be the first to share your thoughts.

Sign in or create an account to comment.