Careers

Careers

Retirement Planning for Information Security Analysts

As a information security analyst, you earn a U.S. median of about $120,000 a year — a solid income by most measures. But a good salary doesn't automatically become a comfortable retirement. That takes two things: using the right accounts for your field, and building a steady saving habit you don't have to think about. This is a complete, plain-English playbook for information security analysts.

Your typical retirement setup

Security analysts typically get a solid corporate 401(k) with a match, and often RSUs or an ESPP. Your field also moves fast, so you'll likely change employers a few times — which makes disciplined rollovers part of the plan.

Whatever your exact plan, the order of operations is the same for most information security analysts. First, contribute enough to capture any employer match — it's an instant, guaranteed return you can't beat anywhere else. Second, fund a tax-advantaged IRA (a Roth IRA if you're eligible) for a bucket of tax-free growth. Third, circle back and push your workplace plan toward the annual limit. Getting that sequence right usually matters more than which specific fund you pick.

What to watch as a information security analyst

- Consolidate as you job-hop. Every move can strand a 401(k). Roll old accounts into an IRA or your new plan so you're not managing five logins and five fee schedules.

- Use the ESPP, then diversify. An employee stock purchase plan is often free money via the discount — but sell promptly and reinvest broadly.

- Automate raises into savings. Security pay climbs fast; bump your contribution rate every time you get a raise so lifestyle doesn't absorb it all.

How much should you be saving?

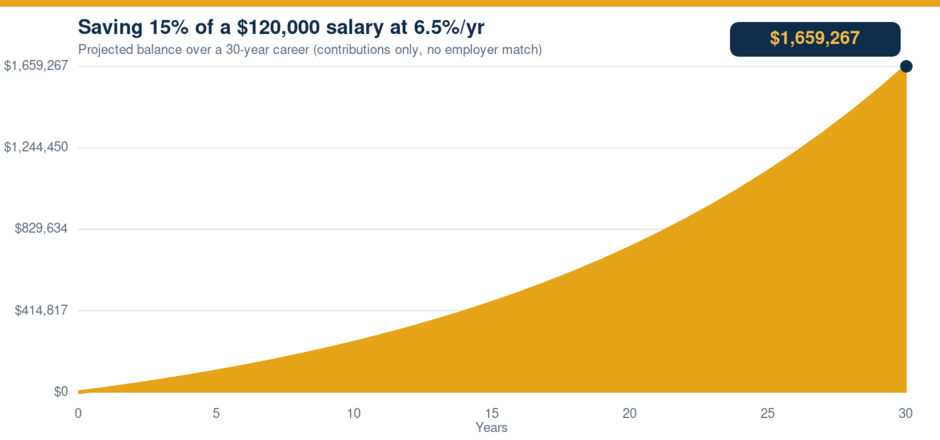

A widely used target is to put away about 15% of your income for retirement, including any employer match. On a $120,000 salary that's roughly $18,000 a year, or about $1,500 a month. If starting at 15% isn't realistic yet, start with whatever you can and raise your contribution rate by one percentage point every year — you'll barely feel it, and the habit is what compounds.

Here's what that steady 15% could grow into over a 30-year career at roughly a 6.5% average annual return — your own contributions only, so an employer match would push the number higher:

That's roughly $1,659,267 from steady saving alone. The shape of that curve is the whole point: the money grows slowly at first, then accelerates dramatically in the later years as compounding takes over. For information security analysts, that means the single most valuable thing you can do is start early and keep going — time matters far more than picking the perfect investment.

Common mistakes to avoid

- Leaving the match on the table. Not contributing enough to get your full employer match is simply turning down free money — usually the highest-return move available to you.

- Cashing out when you change jobs. When you move employers, roll your old account into an IRA or your new plan. Cashing it out triggers taxes, a possible 10% penalty, and the loss of decades of growth.

- Letting every raise become lifestyle. Each raise is a chance to bump your savings rate before the money is spoken for.

- Ignoring fees. A one-percent difference in annual fund fees can cost you six figures over a career. Favor low-cost, broadly diversified index funds and check what you're paying.

- Waiting for the "perfect" time. There isn't one. Automating a modest amount today beats waiting to invest a bigger amount "someday."

Don't overlook catch-up contributions after 50

The year you turn 50, the IRS lets you make catch-up contributions — extra money above the normal limits — into your 401(k)/403(b) and IRA. For information security analysts hitting their peak earning years, this is one of the fastest ways to close a savings gap. If you got a late start, this is your comeback tool.

Your game plan

- Contribute at least enough to capture your full employer match.

- Open and fund an IRA — a Roth IRA if you're eligible — for tax-free growth.

- Automate your contributions and raise them a little every time your pay goes up.

- Keep costs low with broad index funds, and don't over-concentrate in any one stock.

- After 50, use catch-up contributions; review the whole plan with a fee-only fiduciary as your income and complexity grow.

None of this is financial advice — confirm the details for your specific plan or with a qualified professional. But the core is refreshingly simple: use the accounts your career gives you, save consistently, keep your costs low, and let time do the heavy lifting.

Comments

No comments yet — be the first to share your thoughts.

Sign in or create an account to comment.