Age guides

Age guides

How to Save for Retirement in Your 20s: A Simple, Powerful Plan

Saving for retirement in your 20s is the highest-return money move you'll ever make, because you have the one thing income can't buy back: time for compounding. Here's a simple plan — how much to save, why a Roth IRA fits your 20s, and the order to do it in, even on a starter salary and with student loans.

Your 20s feel like the worst time to think about retirement — low salary, student loans, rent. In reality they’re the best time, and it isn’t close. A dollar invested at 25 has forty years to compound; the same dollar at 40 has twenty-five. That head start does more work than a much bigger paycheck later. Here’s exactly how to use it.

Why your 20s are your superpower

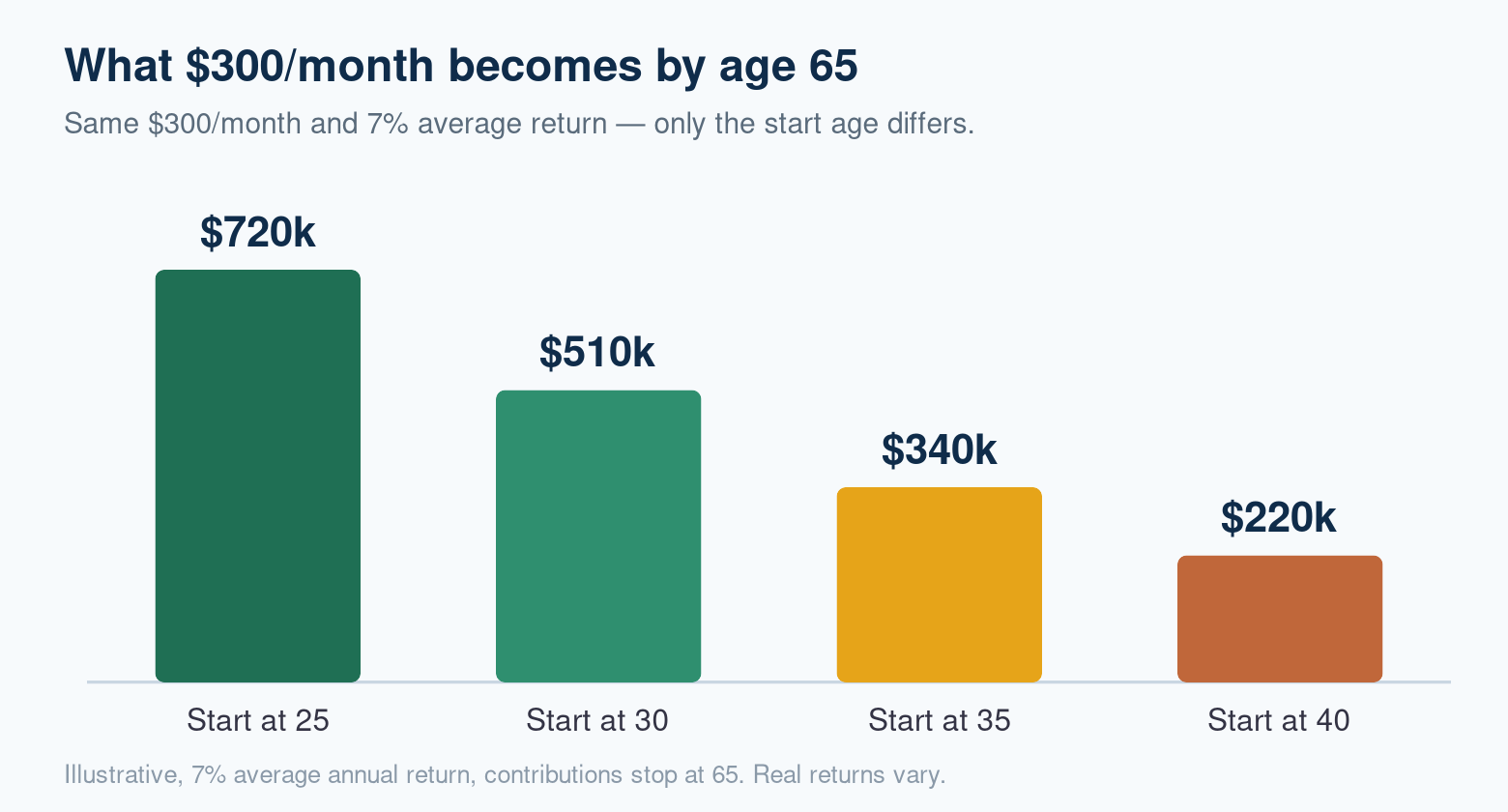

Compounding rewards time even more than the amount you put in. Look at the same $300 a month, invested at a 7% average return, changing only the age you start:

Starting at 25 instead of 35 roughly doubles your ending balance — for the exact same monthly contribution. The person who starts at 25 also contributes more years, but the majority of the gap is pure compounding on that early money. Miss your 20s and you can never fully buy those years back.

How much should you save in your 20s?

A good target is 10–15% of your gross income toward retirement, including any employer match. Can’t hit that yet? Start at whatever you can — even 3–5% — and raise it 1% every year and with every raise. The habit matters more than the number at this stage; a 23-year-old saving 5% is far ahead of a 33-year-old saving nothing.

The order of operations for your 20s

Do these in order — each step earns more than the one after it:

- Starter emergency fund. Save $1,000–$2,000 in cash first so a flat tire doesn’t become credit-card debt. Build it toward 3–6 months of expenses over time.

- Grab the full 401(k) match. If your employer matches, say, 50% up to 6%, contributing 6% is an instant 50% return — the best deal in finance. Never leave it on the table.

- Kill high-interest debt. Credit cards and anything above ~7–8% interest should be attacked next; paying off a 22% card is a guaranteed 22% return.

- Open and fund a Roth IRA. The ideal account for your 20s (see below).

- Go back and max the 401(k) and add taxable investing once the above are handled.

Why a Roth IRA is perfect in your 20s

A Roth IRA is funded with after-tax money, and then all growth and withdrawals in retirement are completely tax-free. In your 20s you’re usually in a low tax bracket, so paying the tax now — while it’s cheap — and never paying it again is a huge win. Decades of compounding come out tax-free. A bonus: you can withdraw your Roth contributions (not earnings) anytime without penalty, so it doubles as a backstop. For most people in their 20s, funding the Roth IRA (up to the annual limit) beats putting extra into a Traditional 401(k) beyond the match.

What to actually invest in

Keep it boringly simple. Inside your Roth IRA and 401(k), choose a low-cost, broad index fund — a total-stock-market or S&P 500 fund — or a target-date fund matched to your retirement year, which auto-diversifies and rebalances for you. In your 20s you can hold mostly stocks; you have decades to ride out downturns, and each dip is buying shares on sale. Avoid stock-picking, day-trading, and high-fee funds — fees are the one headwind you fully control.

But I have student loans

You can do both. Always take the free 401(k) match even while repaying loans — it out-earns the interest on most loans. Beyond the match, compare rates: aggressively pay down anything above ~7–8%, but for lower-rate federal loans it’s usually fine to make regular payments and invest at the same time, because your investments are likely to out-earn a 4–5% loan over decades.

Milestones for your 20s

- By your mid-20s: saving something every paycheck, capturing the full employer match, a starter emergency fund in place.

- By your late 20s: saving 10–15% of income, a Roth IRA open and funded, high-interest debt gone, and roughly half to one year’s salary saved for retirement.

- Always: keep costs low, increase your rate with every raise, and don’t touch it.

Common mistakes in your 20s

- Waiting until you ‘earn more’ — the lost years are the expensive part.

- Leaving the employer match unclaimed (free money).

- Cashing out a 401(k) when changing jobs — roll it over instead.

- Sitting in cash out of fear, or chasing hot tips and crypto bets with money meant for retirement.

- Lifestyle creep: letting spending rise as fast as income so nothing is left to invest.

The bottom line

Retirement planning in your 20s isn’t about big sacrifices — it’s about starting small, automatically, and early. Grab the match, open a Roth IRA, buy a simple index fund, and raise your savings rate over time. Do that, and compounding — not a giant salary — does the heavy lifting. Your future self will retire years earlier because of what you start this decade.

See what your own head start is worth with the compound interest calculator and the retirement savings projection. Review the whole plan with a fee-only fiduciary as your income grows.

Educational information only, not financial, tax, or legal advice. Figures use simplifying assumptions; confirm current contribution limits at IRS.gov.

Comments

No comments yet — be the first to share your thoughts.

Sign in or create an account to comment.