By decade

By decade

How to Plan for Retirement in Your 30s

Two goals, one guide: how to plan for retirement in your 30s, and whether you could actually retire during your 30s. Here's the early-retirement (FIRE) math, the savings rates it takes, and a clear, step-by-step plan to build wealth automatically without sacrificing the life you're building now.

Why your 30s matter more than any other decade

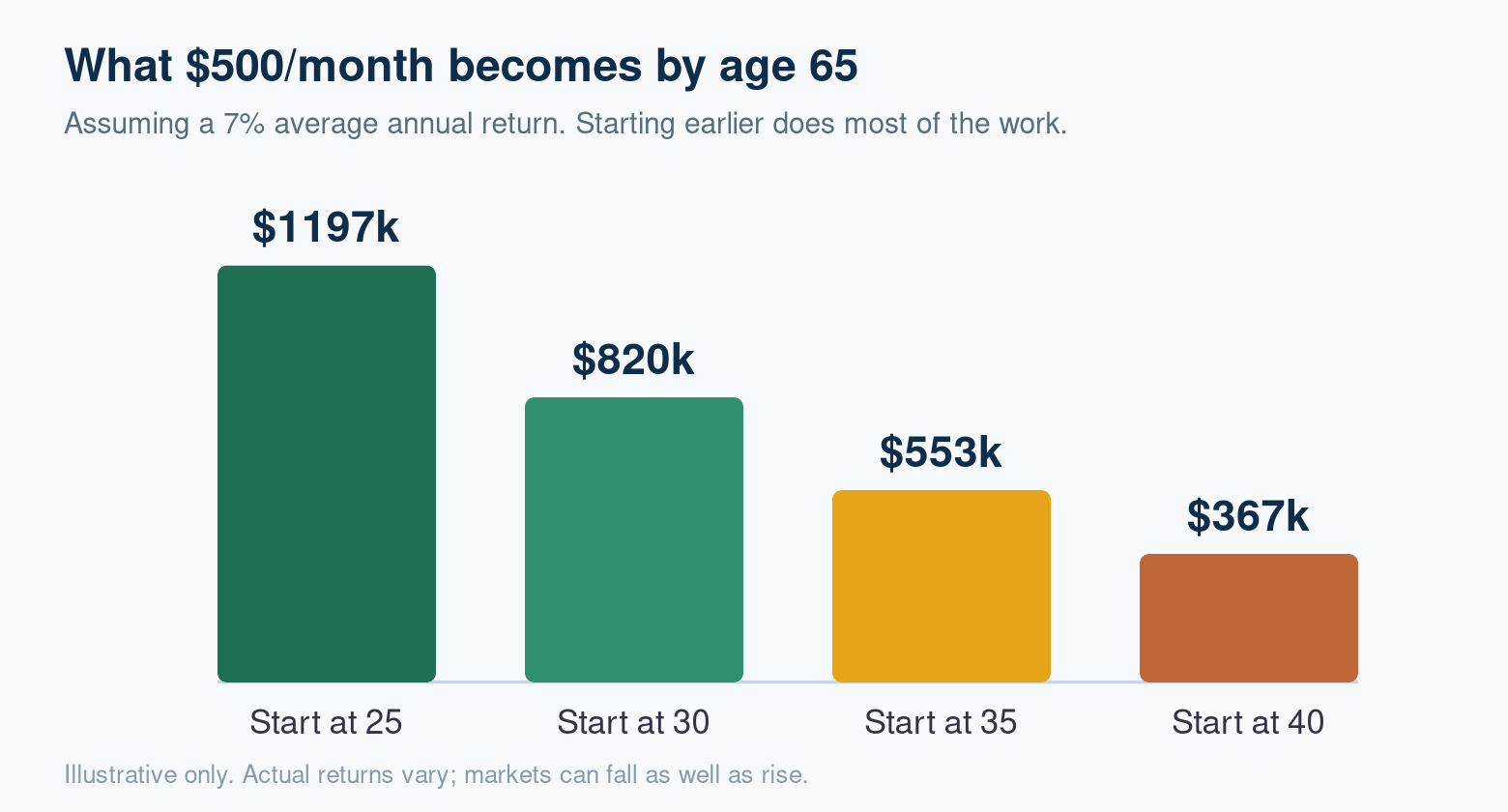

Money invested in your 30s has 30+ years to compound before a typical retirement — and compounding does the heaviest lifting in those early years. A dollar invested at 32 can grow to several times what the same dollar does at 45.

The chart below shows what a steady $500/month becomes by age 65 depending on when you start. The gap between starting at 30 and starting at 40 is enormous, and it’s almost impossible to make up later.

Can you actually retire in your 30s?

Retiring during your 30s — not just saving during them — is the goal of the FIRE movement (Financial Independence, Retire Early). It’s genuinely possible, but it’s a different game from ordinary retirement planning: it runs on an extreme savings rate and a hard number, not on decades of patience.

The whole thing rests on one figure: your annual spending × 25. That’s the nest egg that, under the 4% rule, could cover your expenses indefinitely. Spend $40,000 a year? You need about $1,000,000 invested. Trim spending to $28,000 and the target drops to $700,000 — which is why frugality does double duty: it raises how much you save and lowers the finish line.

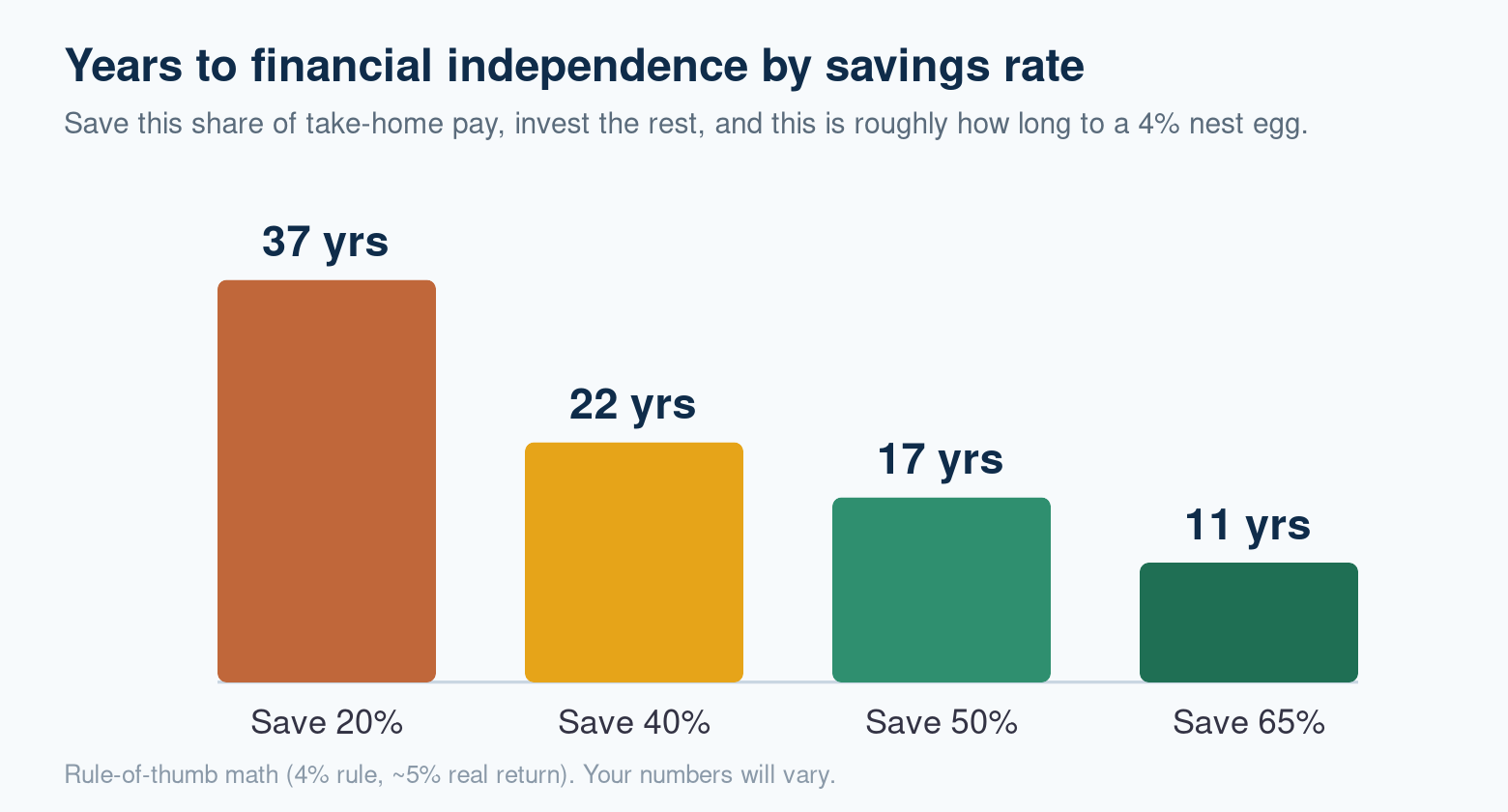

Why your savings rate — not your income — sets the date

Here’s the counterintuitive part: how soon you can retire depends far more on the percentage of your take-home pay you save than on how much you earn. Save 20% and financial independence is decades away; save 50% and it’s in the teens; save 65% and it can be around a decade.

That’s because a high savings rate does two things at once — it builds the nest egg faster and proves you can live on less, so you need a smaller nest egg. The chart below shows the rough relationship.

How people pull it off

- Widen the gap. Financial independence is just income minus spending, invested. Raising income (career moves, side income) and cutting the big three — housing, transportation, food — both widen the gap that gets invested.

- Invest the difference simply. Most early retirees use low-cost, broad index funds in tax-advantaged accounts (401(k), IRA, HSA) plus a taxable brokerage for money they may need before 59½.

- Automate and stay the course. The math only works if the high savings rate is consistent and the investments are left alone through market swings.

The flavors of early retirement

- Lean FIRE: retire on a modest budget with a smaller nest egg — more freedom sooner, less financial cushion.

- Fat FIRE: a larger nest egg funding a comfortable lifestyle — takes longer or a higher income to reach.

- Coast FIRE: save aggressively early, then stop adding and let compounding ‘coast’ you to a normal-age retirement while you work a lower-stress job.

- Barista FIRE: semi-retire — cover part of your costs with light work (often for the health benefits) and the rest from investments.

The hard truths of retiring in your 30s

- A 50+ year retirement is a long time for anything to go wrong. The 4% rule was built on ~30-year horizons; over 50+ years, many early retirees use a more conservative 3–3.5% withdrawal rate for safety.

- Health insurance is the big one. Without an employer plan, you must budget for coverage for decades before Medicare at 65 — often via the ACA marketplace.

- Sequence-of-returns risk. A bad market in your first few retired years is far more dangerous than the same crash later. Cash buffers and flexible spending help.

- Purpose matters too. Many early retirees find they want meaningful work anyway — which is exactly why Coast and Barista FIRE are so popular.

If a full early retirement isn't the goal: your 30s playbook

Most people don’t want to save 60% of their income — and that’s completely fine. You can still set yourself up for a strong, on-time retirement (and keep the option of retiring early open) with a simple, automatic system. Here’s the step-by-step.

Step 1: Build a real emergency fund first

Before aggressive investing, hold 3–6 months of essential expenses in a high-yield savings account. In your 30s — with a mortgage, kids, or a single income — this buffer is what keeps a job loss or surprise bill from forcing you to sell investments or take on debt.

Step 2: Capture the full employer 401(k) match

If your employer matches 401(k) contributions, contribute at least enough to get every dollar of the match. It’s an instant 50–100% return — the best guaranteed deal in investing — and skipping it is leaving free money on the table.

Step 3: Aim for a 15% savings rate (including the match)

A common target is saving about 15% of gross income for retirement, employer match included. If you can’t hit that yet, start where you can and raise your contribution by 1% every year or with every raise — you won’t feel it, and it compounds.

Automate it: money that never hits your checking account is money you never miss.

Step 4: Choose Roth or Traditional deliberately

- Roth (contribute after-tax, withdraw tax-free) is often ideal in your 30s if you expect to earn more later — you lock in today’s lower tax rate and get decades of tax-free growth.

- Traditional (deduct now, pay tax later) can win if you’re in a high bracket today and expect a lower one in retirement.

- Many savers split the difference: enough Traditional 401(k) to grab the match, plus a Roth IRA for tax-free growth.

Step 5: Keep investing simple

You don’t need to pick stocks. A single target-date fund or a low-cost total-market index fund gives instant diversification and adjusts risk over time. Low fees and consistency beat cleverness over 30 years.

Step 6: Use an HSA if you have one

If you’re on a high-deductible health plan, a Health Savings Account (HSA) is triple-tax-advantaged — deductible going in, tax-free growth, and tax-free withdrawals for medical costs. Invested (not just spent) it becomes a stealth retirement account.

Step 7: Balance the big competing goals

- Debt: knock out high-interest debt (credit cards) aggressively; you likely don’t need to rush a low-rate mortgage at the expense of investing.

- Buying a home: keep retirement contributions going while you save a down payment — pausing investing for years to buy a house is one of the costliest 30s mistakes.

- Kids & college: fund your retirement before a 529. Your kids can borrow for college; you can’t borrow for retirement.

Milestones to aim for

A widely used rule of thumb: have roughly 1× your salary saved by 30, 2× by 35, and 3× by 40. If you’re behind, don’t panic — raise your savings rate and let time and compounding close the gap.

Check your progress once a year, increase contributions with raises, and otherwise leave your investments alone.

The bottom line

Whether you’re aiming to retire in your 30s or simply to plan well during them, the levers are the same — you just pull them harder for early retirement. Widen the gap between what you earn and what you spend, invest it simply and automatically, use the tax-advantaged accounts, and let compounding do the rest.

Retiring in your 30s takes an extreme (50%+) savings rate and a tolerance for a very long, self-funded retirement. A comfortable on-time retirement takes far less — mostly just starting now and staying consistent. Either way, your 30s are the most valuable saving years you will ever have, so the best move is to begin today.

A note on where you stand: retirement planning in your 30s is really two jobs at once — building the habit if you are just starting, and knowing how to catch up on retirement savings in your 30s if you feel behind. Neither is too late. A decade of steady, tax-advantaged saving in this window still compounds powerfully into your 60s.

Educational information only — not financial, tax, or legal advice. Consult a qualified professional about your situation.

Comments

No comments yet — be the first to share your thoughts.

Sign in or create an account to comment.