By decade

By decade

Catching Up on Retirement in Your 40s (When You Didn't Plan)

Behind on retirement in your 40s? You're not out of time — with 20+ years left, an aggressive savings rate, catch-up contributions, and a few focused moves can still build a real nest egg. Here's a step-by-step catch-up plan for people who didn't get an early start.

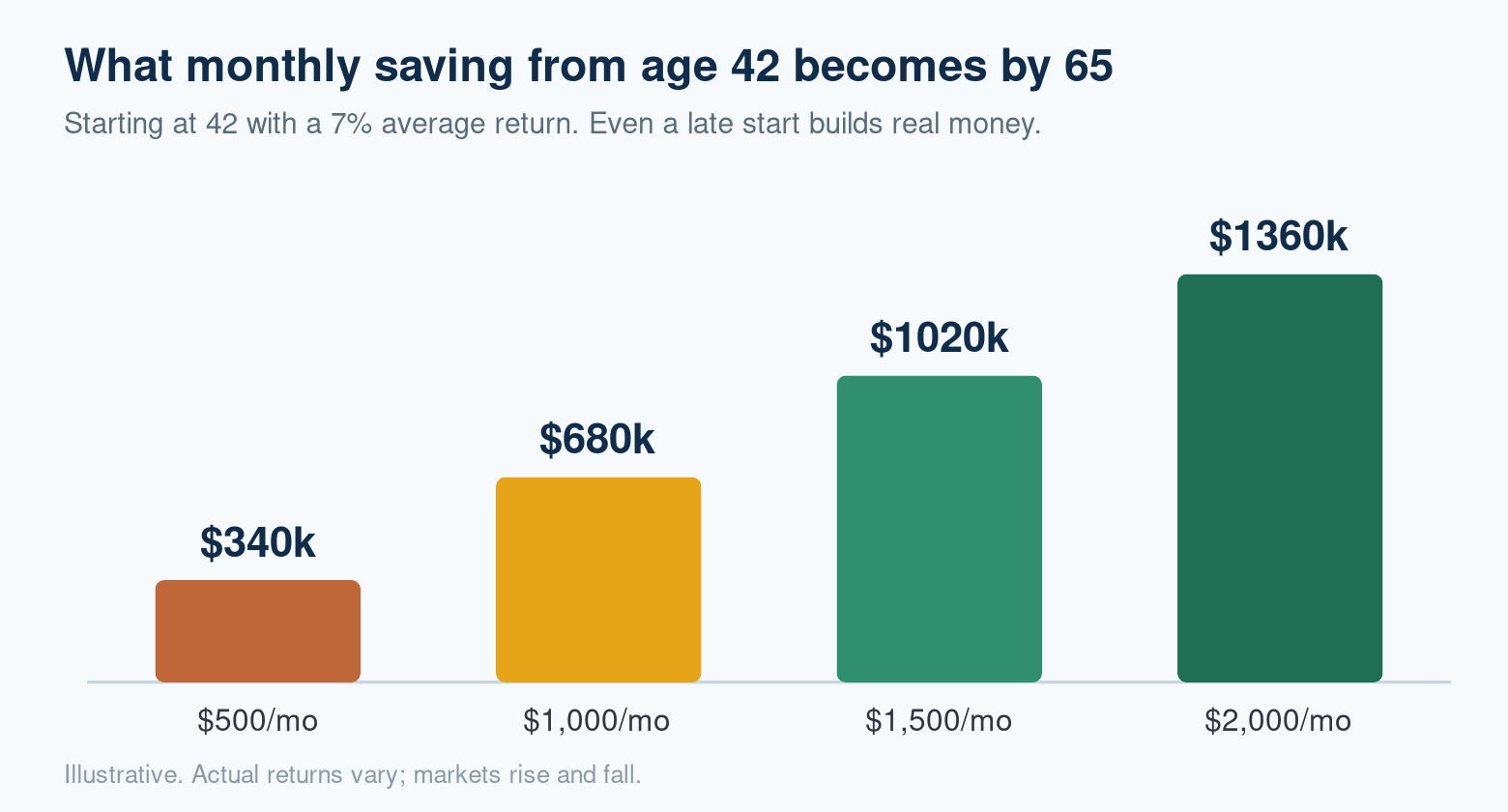

If you hit your 40s and realize you barely saved for retirement, take a breath: you have not missed the boat. A 42-year-old still has around 23 years until a normal retirement — enough time for disciplined saving and compounding to build a meaningful nest egg. The chart below shows what’s still possible.

First, face the real numbers

Progress starts with an honest baseline. Add up what you have across every 401(k), IRA, and account. A common benchmark is having about 3× your salary saved by 40. If you’re under that — most people are — don’t panic; just treat the gap as the target you’re now closing.

The catch-up playbook

- Grab the full employer match today. It’s an instant 50–100% return — the fastest catch-up move there is.

- Crank your savings rate. The standard 15% may not be enough on a late start; aim for 20–25%+ of income if you can. This is the single biggest lever you control.

- Use catch-up contributions. At 50+, the IRS lets you add extra to 401(k)s and IRAs — and a new SECURE 2.0 ‘super catch-up’ lets ages 60–63 add even more. Plan to use every dollar of it.

- Save in your peak-earning years. Your 40s and 50s are usually your highest-income years — direct raises and bonuses straight into retirement instead of lifestyle.

- Kill high-interest debt. Paying off a 20% credit card is a guaranteed 20% return — do it before chasing investment gains.

- Right-size the kids’ college. Fund your retirement before a 529. Your children can borrow for school; you can’t borrow for retirement.

- Consider working a couple of extra years. Delaying retirement from 65 to 67–70 adds saving years, shortens the years you must fund, and boosts Social Security — a triple win that can dramatically de-risk a late start.

Keep the investments simple

A late start is not the time to gamble to ‘make up’ ground — big bets can just as easily set you further back. Stick with a diversified, low-cost index fund or target-date fund, keep fees low, and let consistency do the work.

The bottom line

Starting late is a disadvantage, not a dead end. Save aggressively, capture every match and catch-up dollar, kill high-interest debt, and consider a slightly later retirement — and a 40-something who didn’t plan can still retire comfortably. The best day to start was 20 years ago; the second-best is today.

See where you stand with the free Retirement Portfolio Analyzer.

Educational information only, not financial advice. Examples use round assumptions to illustrate the math; your situation will differ. Consider talking to a qualified professional.

Comments

No comments yet — be the first to share your thoughts.

Sign in or create an account to comment.